Roof Depreciation Rate

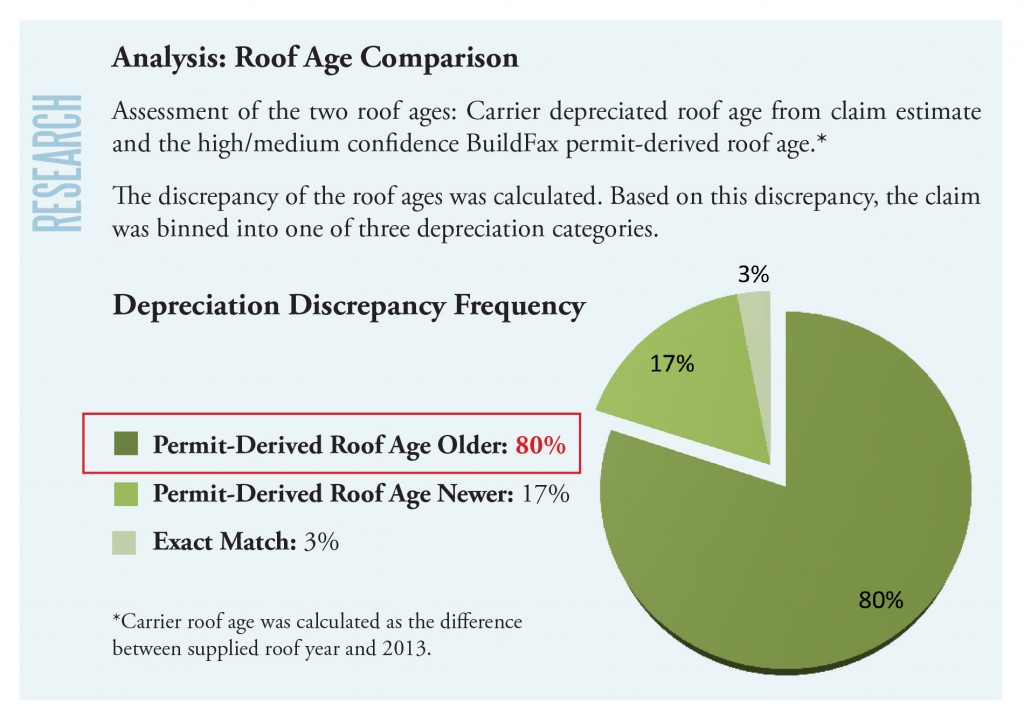

Part Three The Value Of Accurate Roof Age In Claims

What Recoverable Depreciation Means And How To Calculate It

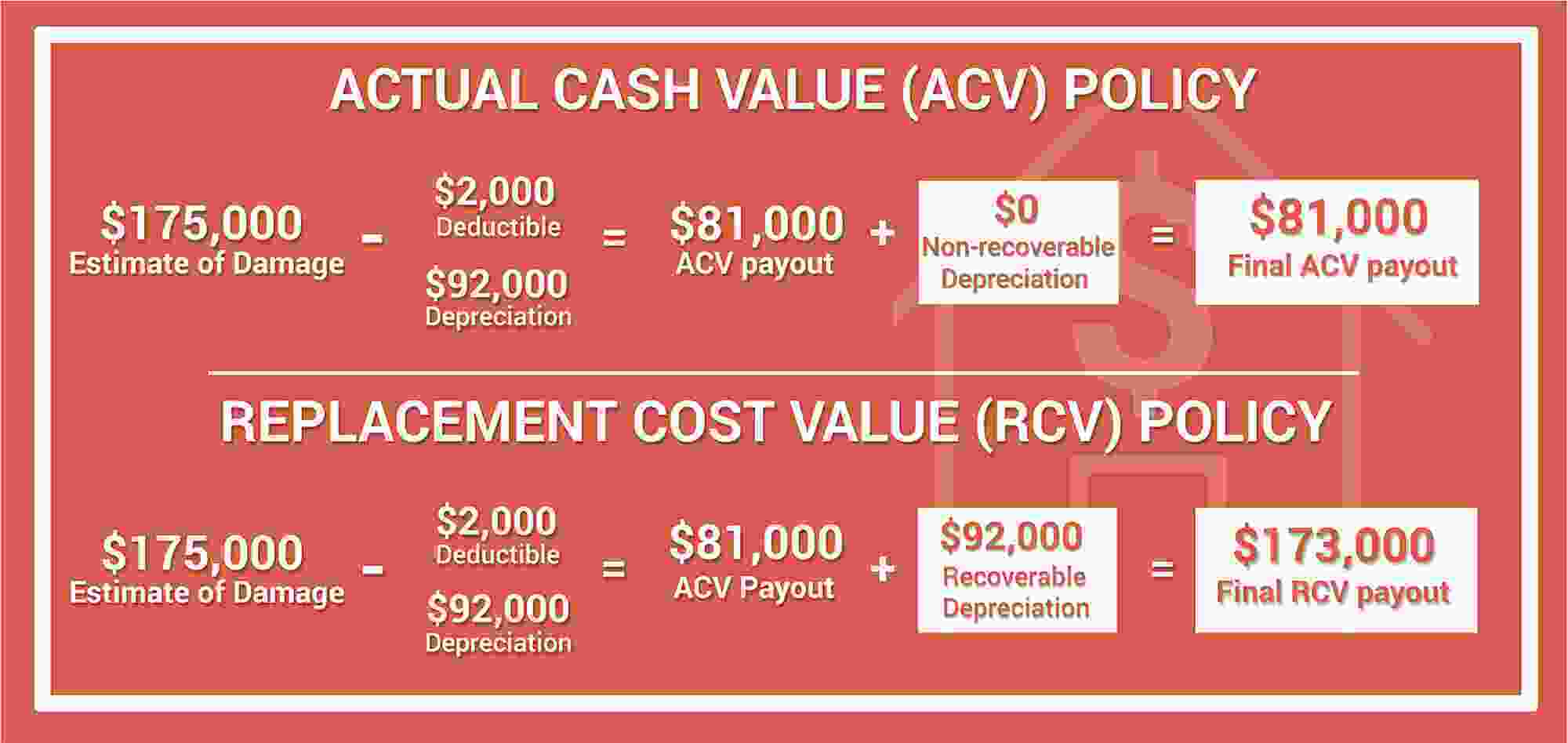

Replacement Cost Value Rcv Vs Actual Cash Value Acv

Calculating Roof Depreciation In An Insurance Claim The Voss Law Firm P C

How To Understand Depreciation On Your Roof Insurance Claim

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

Is generally depreciated over a recovery period of 27 5 years using the straight line method of depreciation and a mid month convention as residential rental property.

Roof depreciation rate.

How Recoverable Depreciation Works

Actual Cash Value The 15 Year Roof Rule Cw Roofing Construction

The Average Depreciation Rate Of A Vehicle Small Business Chron Com

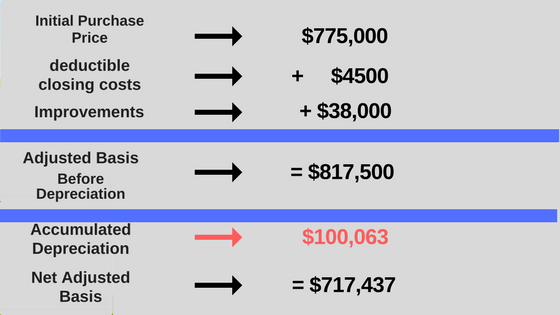

How Rental Property Depreciation Works The Benefits To You

Acv Vs Rcv Office Of Public Insurance Counsel Opic

What Is The Depreciation Of The Roof On A Commercial Building

Actual Cash Value Vs Replacement Cost Value Florida Insurance Claim Lawyers

Give Me My Recoverable Depreciation

Roof Insurance Acv Vs Replacement Cost Bankrate

Calculating Your Profit When Selling Your Rental Property Mortgage Blog

How Does Recoverable Depreciation Impact My Home Insurance Claim Valuepenguin

Homeowners Insurance 101 Roof Age Matters At Claim Time

Section 179d Tax Deduction For Commercial Roof Replacements

Health Depreciation Rate With Age And Health Investment Download Scientific Diagram

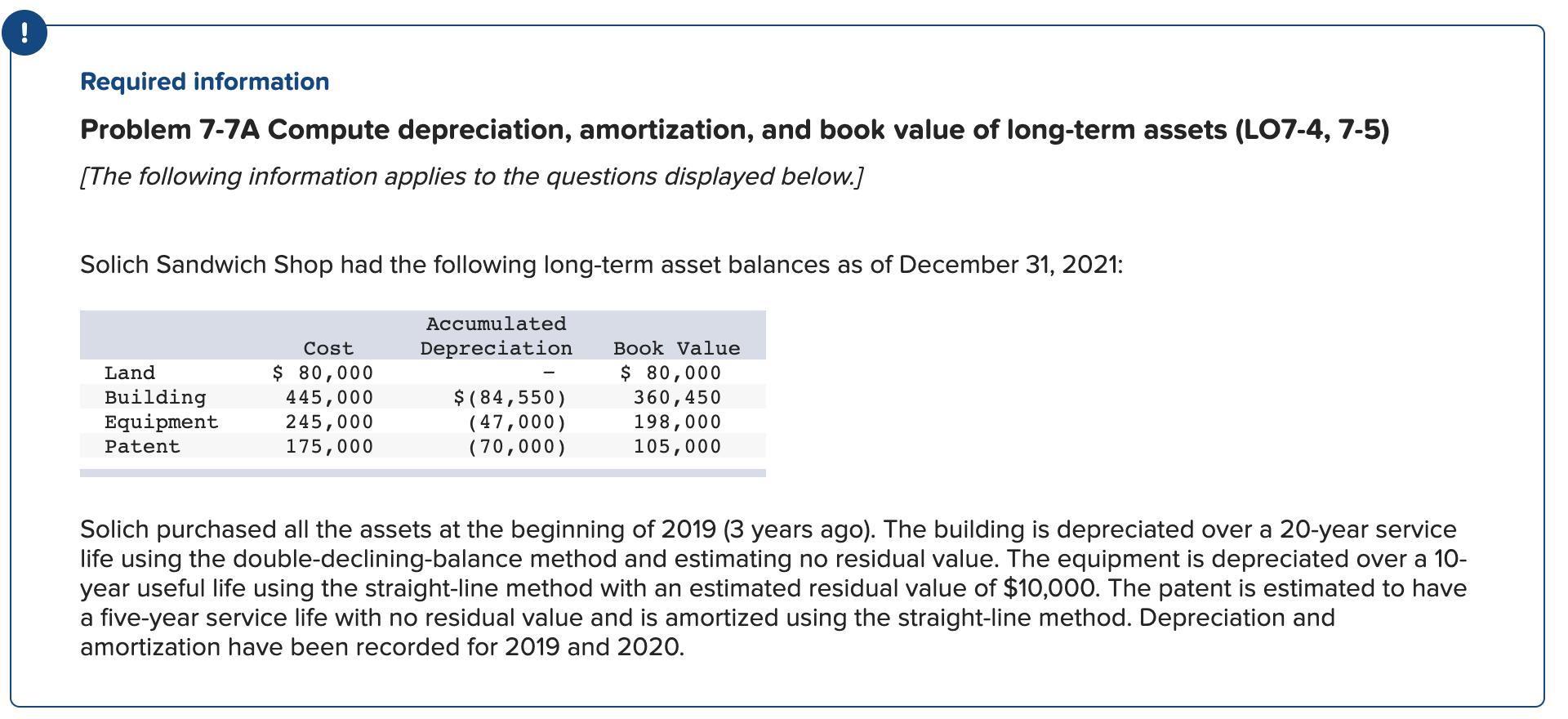

Solved Problem 7 7a Compute Depreciation Amortization A Chegg Com

What Is Withheld Depreciation Charlotte Insurance Blog

Actual Cash Value Is The Cost Of Labor Part Of Depreciation The Courts Are Divided Insurance And Reinsurance Disputes Blog

Jake S Roof Repair Has Provided The Following Data Concerning Its Costs Fixed Cost Per Month Cost Homeworklib

Green Roof Financing Program

How To Calculate Rental Property Depreciation Morris Invest

Heatspring Magazine Finance 101 For Solar Pv Professionals

Can I Make Money Off My Insurance Roofing Claim Slade Roofing

Navigating The Roofing Insurance Claim Process Pdf Free Download

Depreciating Labor Costs The Rough Notes Company Inc

Source : pinterest.com